yahoo Press

Mortgage interest tax deduction for homeowners: Is it worth it?

Images

1 / 12

2 / 12

3 / 12

4 / 12

5 / 12

6 / 12

7 / 12

8 / 12

9 / 12

10 / 12

11 / 12

12 / 12

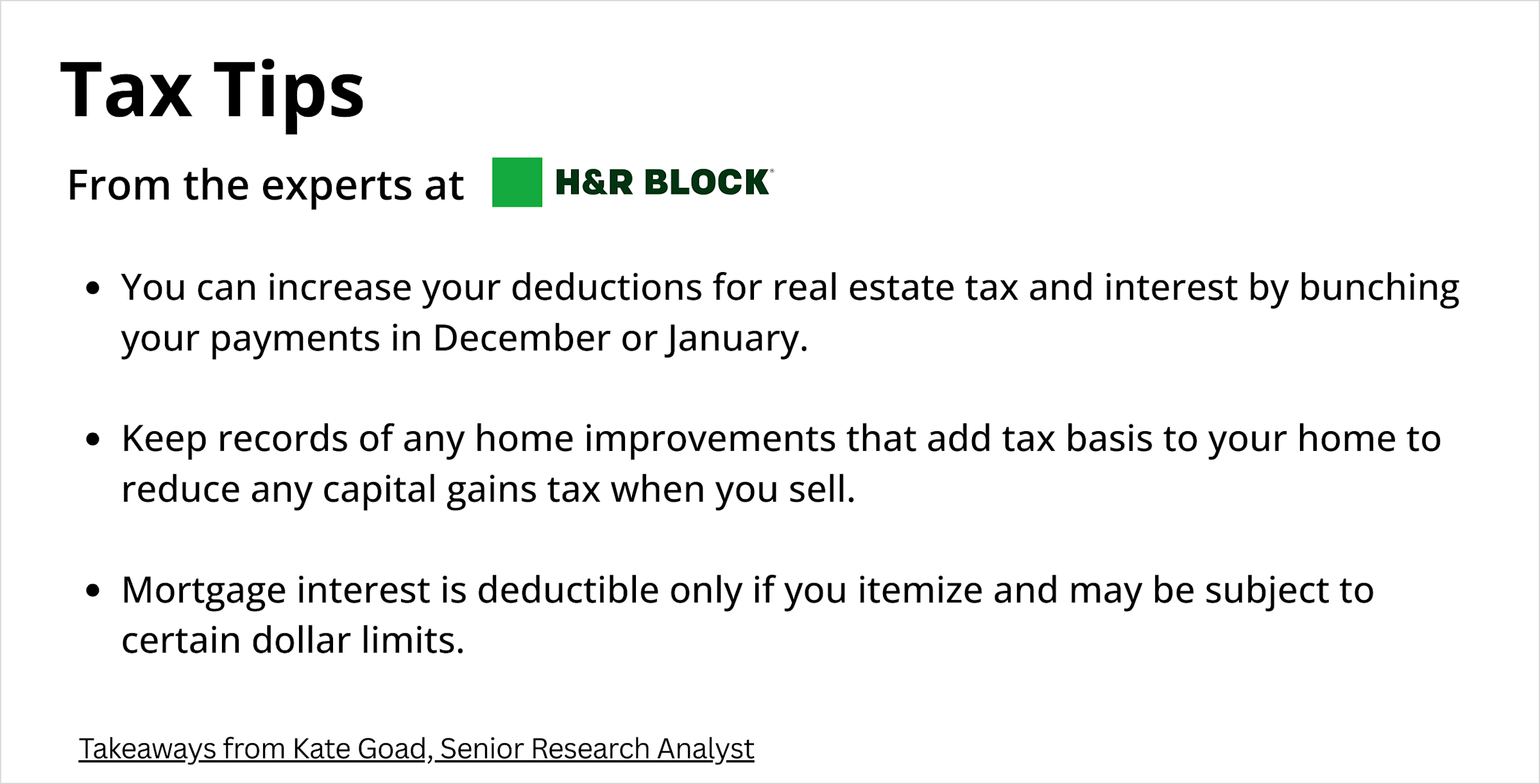

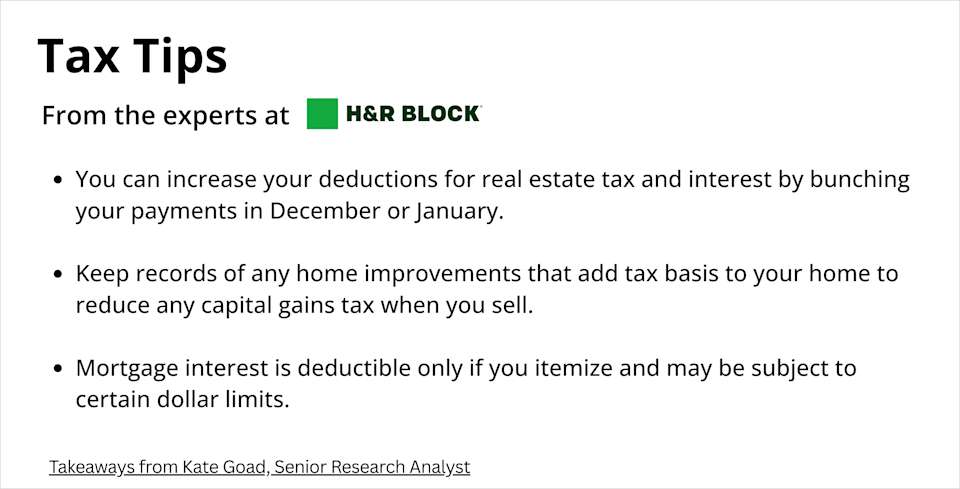

If you’re among the 60% of Americans with a mortgage, you might have heard there’s a tax break waiting for you: the mortgage interest deduction. Well, that used to be more true than it is today. Over the past several years, the rules around this write-off have changed in two significant ways: loan limits have dropped, and the standard deduction has increased. So, you might qualify to deduct your mortgage interest on your taxes this year — as long as you meet certain IRS guidelines. Here’s how it all works. At a basic level, yes. You can deduct mortgage interest for certain loans on your 2025 tax return, but there’s a catch: You’ll have to itemize to catch this tax break. If you itemize, you can deduct interest paid during the 2025 tax year on up to $750,000 of what the IRS calls “home acquisition debt.” In plain English, that means money you borrowed to buy, build, or make substantial improvements to your primary or secondary home as long as that property secures the loan. That means interest paid on a personal loan you took out for a kitchen remodel doesn’t qualify. Steven Elliott, tax director at Mercer Advisors, said the lower limit is one of the most significant long-term changes from the Tax Cuts and Jobs Act of 2017. “The TCJA lowered the maximum mortgage interest deduction amounts from $1,000,000 to $750,000 for primary residences,” said Elliott in an email interview. “The One Big Beautiful Bill Act made the $750,000 amount permanent in the law.” That permanence matters. The deductible mortgage interest limits set by the TCJA were scheduled to expire at the end of 2025. If they had, the loan limits would have jumped back up to $1 million. However, the OBBBA passed before the end of 2025 and made the TCJA limit permanent. Now, only certain mortgage holders can deduct up to the previous $1 million loan limit, which we’ll get to in a minute. For now, let’s focus on an important nuance of the new $750,000 limit: That’s $750,000 in total, not per eligible property. If you have a $700,000 mortgage on one property and a smaller mortgage of $100,000 on a secondary property, you don’t get to deduct the mortgage interest on $800,000. You’re still subject to the $750,000 cap for single and joint filers. Married filing separately couples can each deduct interest on up to $375,000 in loans. Have rental property? That’s a different animal. Mortgage interest on rental properties is generally deducted as a business expense, not under these personal-use rules. Learn more: 4 ways the One Big Beautiful Bill Act could lower your taxes Now, let’s go back to the $1 million mortgage interest deduction cap that was in place before the 2017 TCJA. If you have a mortgage on a primary or secondary residence that originated before Dec. 15, 2017, you can itemize and claim the interest paid on qualifying loans up to $1 million. It’s important to know, however, that you have to keep those mortgages to remain eligible for that higher cap. If you refinance, you’re subject to the new $750,000 cap set by recent legislation. Let's say you bought a home in 2016 with an $850,000 mortgage. Under the pre-TCJA rules, you’re still well under the $1 million cap and could potentially deduct all your mortgage interest paid in a year using an itemized return. But say you fast-forward to 2022 and do a cash-out refinance that brings your new mortgage to $900,000. Now, you’re subject to the lower $750,000 TCJA/OBBBA cap. You now have a higher mortgage amount, but lose the ability to deduct interest paid on $150,000 of that new loan balance. Misunderstanding how refinancing affects your tax deductions can definitely create filing errors. Elliott says he still sees tax returns prepared by those who have refinanced and still think they qualify for the higher cap. Sadly, they don’t. Even if you fall within the new loan limits enshrined by the OBBBA, you still only benefit from the mortgage interest tax deduction if you itemize your return instead of taking the standard deduction. And since 2018, the standard deduction has increased. Back in 2018, the standard deduction was $12,000 for single filers and $24,000 for joint filers. Today, the standard deduction is up to $15,750 and $31,500, respectively. While that might not seem like a big jump, it matters more to the everyday taxpayer than to high earners with substantial mortgages. An individual has to come up with $15,751 in deductible expenses before itemizing makes financial sense. Married couples? Double that. Let’s look at two examples: a $250,000 mortgage and a $400,000 mortgage. $250,000 30-year fixed-rate mortgage at 6.09% Monthly payment: $1,513 Interest paid, year one: $15,142 Difference between mortgage interest and standard deduction: -$608 Should you itemize? Likely not, unless you have significant other deductions that would add up to more than the $15,750 standard deduction for single filers. If you’re filing jointly, likely not. $400,000 30-year fixed-rate mortgage at 6.09% Monthly payment: $2,421 Interest paid, year one: $24,277 Difference between mortgage interest and standard deduction: $8,527 Should you itemize? Likely, since additional expenses like charitable donations and state and local taxes (SALT) could add to your savings as a single filer. If you’re filing jointly, likely not. If you’re filing jointly, it would take a minimum mortgage of $550,000 to $600,000 at the above rate and term to make itemizing to claim the mortgage interest deduction worth it. Home equity lines of credit (HELOCs) and home equity loans have long been popular ways for homeowners to leverage their equity to cover various expenses. Whether the interest on those lending products is tax deductible depends on how you use the funds. “Since 2018, interest on HELOCs or home equity loans is ONLY deductible if the funds are used to buy, build or substantially improve the home that secures the loan,” said Elliott. “There is also tracing required for the use of the proceeds.” Tracing means documentation. So, if you took out a HELOC for $100,000 and used $70,000 for a kitchen remodel and $30,000 to pay off credit cards, only the interest on the $70,000 is tax deductible. Plus, you’ll need to keep the receipts to back up how you used that $70,000. If you do a cash-out refinance to tap your home equity, the same logic applies. If you use the extra cash from your equity for a vacation, a new car, or college tuition, the interest isn’t deductible. If the math makes sense for you to itemize to claim the mortgage interest deduction, claiming it isn’t all that complicated. You’ll get a Form 1098 from your lender that clearly states how much interest you paid. You’ll put that number on Schedule A, Itemized Deductions. Before filing, however, it’s worth it to run the numbers using both the standard and itemized deductions. Whether you use online tax prep software or a tax professional to file, it’s easy to get a look at both scenarios. From there, you can decide which one brings you the lower tax bill. Read more: Everything you need to know about the new IRS Schedule 1-A tax breaks The answer to this one is tricky. First, you’ll need to itemize deductions on your tax return to claim your mortgage interest. Then, you’ll only be able to deduct interest up to the allowable IRS cap on your primary and/or secondary home. For tax year 2025, that cap is generally $750,000 for single and joint filers and $375,000 for anyone married filing separately (for mortgages originated after Dec. 17, 2017). If you took out your mortgage before that date, the cap can be as high as $1 million. Consult a tax advisor to see how much of a deduction you might qualify for. For the 2025 tax year, homeowners can generally deduct between $750,000 and $1 million in mortgage interest — as long as they meet certain IRS qualifications. To start, you can only deduct interest on your primary and/or secondary homes. Next, you’ll have to skip the standard deduction and itemize to capture this tax break. Then, how much you can deduct depends on your filing status and when you took out your mortgage. For loans originated on or after Dec. 17, 2017, single and joint filers can deduct up to $750,000 in mortgage interest ($375,000 for married filing separately). For loans originated before Dec. 17, 2017, that cap goes up to $1 million ($500,000 for married filing separately). It can totally be worth it to claim mortgage interest on your taxes so long as the math works out. To make it worth it, the total of your itemized deductions will need to be more than the standard deduction. If you have significant deductions like charitable giving and state and local taxes (SALT), those things added to your mortgage interest can quickly add up to more than the standard deduction. However, if the standard deduction is still more than the total of your itemized deductions, it makes more financial sense to take the standard deduction. Running the numbers is key. Interest paid on a home equity loan may be tax deductible if you use the funds for specific purposes. Find out whether you qualify for this deduction. Homeowners face new tax rules in 2026 under the OBBB. Here's what's new, plus 8 deductions homeowners should know about. Mortgage points can be tax-deductible, but you must meet the requirements, itemize your deductions, and heed certain limits. Here’s how to deduct your mortgage points. The One Big Beautiful Bill Act comes with a slew of updates affecting U.S. homeowners. It's worth taking a new look at whether you should itemize. Interest paid on a HELOC is tax deductible, but there are limits on how to spend the money to qualify for a deduction. Learn how to deduct HELOC interest. Homeowners face new tax rules in 2026 under the OBBB. Here's what's new, plus 8 deductions homeowners should know about.